Scammed

Image: US Attorney's Office

“I THINK WE ALL have a little greed in our heart.”

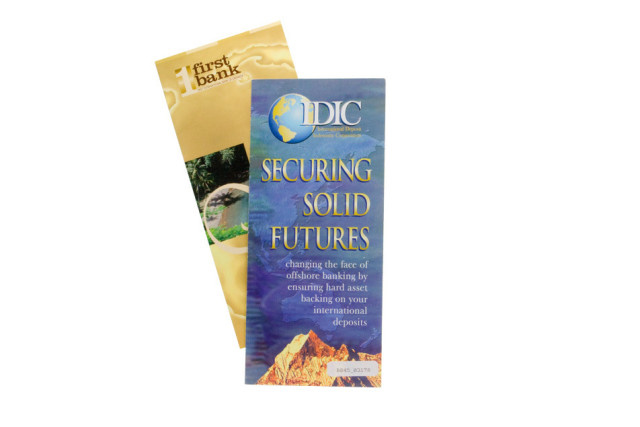

John Turnquist, a silver-haired, 72-year-old grandfather, is having a cup of coffee in the kitchen of his floating house on the Columbia River. This is his explanation for why, one day back in 1999, he sat down, made a check out to the First International Bank of Grenada, and then mailed it to an address on the Caribbean island of Antigua. He figured he was about to hit payola. He’d just received $10,000 from his mother’s estate, and, as anyone might, he wanted to parlay this minor windfall into an interest-bearing investment. A friend told him about a great opportunity, a newly formed offshore bank that promised staggering annual returns of 20 percent or more, guaranteed. Any of Turnquist’s doubts might have waned when he saw the prospectus from the bank, which was based in the Grenadian capital of St. George’s. The glossy 28-page brochure featured paradisiacal pictures of cerulean waters and beaches lined with palm trees, each image punctuated by an inspirational quote: Realize your hopes, dreams, and ambitions. Offshore investing: legal, safe, simple, and wise.

“It was very professional-looking,” he says. But what clinched it for him was a second pamphlet from the International Deposit Indemnity Corporation, or IDIC, a multibillion-dollar, multinational insurance corporation, which guaranteed that both Turnquist’s investment and any interest it earned were safe.

A few weeks after he mailed in his check, Turnquist received a certificate of deposit signed by the bank’s CFO, Rita Regale. Not only did he not receive any returns, but he never saw a penny of his $10,000 again.

But Turnquist was one of the luckier ones. One local man invested his mother’s entire pension fund—$15,000. Turnquist mentioned the deal to a golf buddy—who then lost nearly $100,000. A Portland salesman who’d hoped to retire on the interest he earned on his $200,000 investment lost everything; at 68, he’s trying to start a new career as a website designer.

All of them were victims of what became the largest financial fraud case ever prosecuted in Oregon, a shell game so complex that it took the US Attorney’s Office in Portland nearly nine years to unravel the morass of money-laundering schemes, illegal banks, sub-banks, fake investment companies, and nonexistent investment funds that eventually bilked some 4,000 people in at least eight countries out of at least $170 million—and probably millions more.

In August of last year, federal prosecutors finally put away four of the scam’s ringleaders. All are now serving sentences in federal prison. But even they claim to be victims, duped by a Hillsboro man named Gilbert Ziegler, aka Van Brink, who proved to be one of the greediest, and best, con men in Oregon’s history.

In March 1998, a securities investigator for the Oregon Department of Consumer and Business Services named Bill Karalekas slipped to the back of a rented conference room in a Lake Oswego condominium complex to watch a presentation about an offshore investment fund called Private Legacy Trust. A week earlier, a pastor at a small Tigard church had called Karalekas’s offices with a complaint: Some of his parishioners had invested with Fidelity International Bank, located on the island of Nauru, but the interest on their money never materialized. Karalekas’s staff called the Office of the Comptroller of Currency on Nauru, which said that the bank had no authority to conduct offshore banking business there.

Packed into the room were some 80 people, Karalekas recalls, many around retirement age and all of them atwitter with excitement. Word about Gilbert Ziegler’s incredible investment had already gotten around, and the buzz in the room was palpable. They sat in small groups, whispering to each other and flipping through the fund’s dazzling prospectuses and brochures.

When Ziegler arrived—the crowd believed him to be the president of Fidelity International Bank—they broke into applause. After waving at a few familiar faces, Ziegler, who wore a flowered shirt and a gold necklace, announced that he’d just flown in from Hawaii. “He tried to project that he was a bon vivant kind of guy,” Karalekas recalls. “He was very confident.” But Ziegler also portrayed himself as a regular person—someone just like them, but one who also happened to be a multimillionaire.

For the next hour, Ziegler strode back and forth, giving his pitch, smiling in earnest, explaining the beauty of his risk-free investment opportunity: By purchasing a 10-year $10,000 Private Legacy Trust CD with Fidelity International Bank of Nauru, each and every person in the room would get a 20 percent annual return on the money. Of course, they could always invest more, which would net even greater returns. Best of all, their money was 100 percent safe. The bank was backed by the IDIC after all, and it had $101 billion in assets.

During the Q&A period, no one asked why a bank president presiding over billions of dollars might take the time to deliver a pitch to low-level investors in a rented conference room. “Most of them were gullible; they wanted to believe,” says Karalekas. Not one person wondered out loud whether it was too good to actually be true. Ziegler was a man who had learned how to build real wealth, and who now, out of the goodness of his heart, wanted to share this good fortune with others. After the presentation, attendees broke into groups to pore over paperwork.

Karalekas immediately recognized the pitch as a scam—and a likely Ponzi scheme. Named after Carlo Ponzi, an Italian immigrant who in 1920 defrauded thousands of people by offering a 40 percent return if they invested in his international postage-stamp program, Ponzi schemes pay back “interest” with money scammed from new investors—payments that eventually stop coming.

A couple of weeks later, Karalekas attended another Fidelity International Bank pitch meeting, this one in a rented office in a Tigard strip mall, where specific questions from investors were waved away with the explanation that “a lot of things are confidential.” In June 1998, Karalekas and the Tigard police raided these offices, taking computers and papers. They soon found evidence of securities fraud, mail fraud, and wire fraud, as well as the names and addresses of hundreds of investors. It also turned out that investors’ checks had crossed not just state lines, but international borders, all of which meant that a state investigation was now a federal one that had to be turned over to the US Department of Justice.

It was not the first time that Gilbert Ziegler had drawn attention from the justice department. In the early 1990s, Ziegler owned the Hillsboro-based Hometown Mortgage Corporation, where he proved to be less than capable of running a business. After the Oregon Department of Justice received numerous complaints from Ziegler’s clients, who accused him of overcharging, they investigated the company. Although Ziegler denied the allegations, he signed an Assurance of Voluntary Compliance, in which he agreed not to conduct business as a mortgage or loan broker in Oregon again. In debt for more than $1.1 million, he declared bankruptcy and then decamped for Hawaii, where, as he would later tell would-be investors, he was struck by a vision “inspired by God Himself” while walking on the beach in Maui: He should start an offshore bank.

The business climate in the Caribbean was perfect for realizing such a dream. Places like the Cayman Islands had hosted offshore banks since the 1960s—they had transformed a country that was little more than specks on a map into one of the world’s largest financial centers. Because the Cayman Islands doesn’t tax corporate income or earned interest, its offshore banks have flourished (today more than 275 banks are registered there). As a result, legions of wealthy investors flock to the islands, turning them into tropical playgrounds for the rich.

Eager to cash in on the boom, poorer Caribbean islands like Dominica, Nevis, and St. Vincent announced in the 1990s that they, too, would officially open their doors to offshore banking, but these governments were entirely ill-equipped to manage the complexities of the industry. They created banking rules on the fly; rarely enforced them; rarely tried to verify a bank’s legitimacy. Corruption was commonplace, bribery of officials endemic. As a result, the Caribbean also became the go-to place for con artists. David Marchant, the editor of OffshoreAlert, a watchdog newsletter about the offshore banking industry, likens Caribbean offshore banking in the 1990s to “the Wild West, with the same people setting up the same scams, watching them collapse, and setting up again.”

Ziegler wanted in on it. In August 1996, he bought the rights to Fidelity International Bank, which was an offshore bank in name only, for $50,000. He then began to perfect his investment pitches in Hawaii and later in Oregon, explaining to rapt vacationers that offshore banking was the only place to invest. Why would anyone put their money into a 401(k) with wimpy yields of 6 percent when they could be making triple and quadruple that—tax free—by investing in Fidelity International? In October 1996, he created a fraudulent loan application for $750,000 against the home of his colonic therapist so that she, too, could invest in Fidelity, promising her a 50 percent return. He then began making “interest payments” on her $300,000 investment in Fidelity with her own money.

Earlier in the year, Grenada, one of the poorer islands in the Caribbean (its economy depended primarily on the export of nutmeg, cocoa, and mace) had announced that it, too, would begin offering licenses for offshore banks. In the fall of 1997, Ziegler’s brother, James, claiming the investments of Fidelity International Bank as assets, flew to Grenada and secured a “certificate of incorporation.” The Zieglers called their new bank the First International Bank of Grenada, or FIBG; as its name suggests, it was the first bank on the island.

So ineffective was Grenada’s government that, according to OffshoreAlert, Gilbert Ziegler may have traveled to the country with a passport naming him the Ambassador at Large for the Dominion of Melchizedek, a fake country that existed only on the Internet and was created by con artists for other cons. (His own US passport was valid, but having a second one made him more difficult to trace.) Although Grenada required $2.25 million in capital to set up an offshore bank, Ziegler provided only about $110,000, promising to pay the rest later, terms Grenadian officials accepted.

First Bank, as it was known, eventually rented space on the second floor of a run-down, whitewashed building on Young Street in the capital city of St. George’s, a quaint town of 7,500 where colorful colonial buildings are set on the edge of a blue lagoon. Ziegler and his staff began working the phones from the bank’s offices, first by calling people in the United States and Canada who’d previously invested in Fidelity International, to let them know about new Grenadian investment opportunities. These included the Super NEWPP fund (for “No Early Withdrawal of Principal Permitted”), which required a minimum $1 million deposit and on which the investor would earn 250 percent at the end of a five-year term.

By April 1998, the money started to pour in, and First Bank’s employee roster eventually swelled to some 50 people, including many locals who answered phones and did the bank’s clerical work. Ziegler also had installed a board of directors, among them Rita Regale, a former grocery-store manager he’d met in Hawaii. Though she never went to college, Regale served as First Bank’s chief financial officer and was charged with signing all of the bank’s certificates of deposit and managing the database of investor names. Ziegler’s longtime associate Douglas Ferguson, who managed a dry-cleaning business in Oregon, headed up the International Deposit Indemnity Corporation (IDIC), which was modeled after the US Federal Deposit Insurance Corporation and which Ziegler used as a tool to boost investor confidence. (In fact, IDIC, a business name registered on the island of Nevis, was nothing more than a fax machine set up in a lawyer’s office on the island of Dominica.) Robert Skirving, a former Amway salesman from Portland, was put in charge of creating new schemes to bilk investors. And Laurent Barnabe, who in 1995 pleaded guilty to selling unregistered securities in Canada, acted as chief operating officer; his task was to develop First Bank’s seminars and glossy marketing materials and create dozens of fraudulent funds and sub-banks that made clients’ money extremely difficult to track.

Newsletters. Direct solicitation. Word of mouth. Internet. First Bank employees went into overdrive. They set up fake businesses like the Offshore Educational Institute, where investors could learn about the advantages of offshore investing. They established a program called Granite Registry Services, through which people would make deposits via “international business corporations”—a way of making the money more difficult to trace. They hired a network of salesmen who worked for the bank’s “Asset Research and Development Association,” and who would get a cut out of every investment procured. They tried their hand at pyramid schemes with the Given in Freedom Trust program, and cross-marketed their fraudulent programs with other fraudulent offshore businesses. They even created a fake stock exchange—the World Investors Stock Exchange, or WISE—where people could purchase stocks in offshore companies guaranteed and backed by First Bank.

Of course, much of the money collected ultimately ended up in numerous bank accounts that afforded the First Bank “board of directors” a very good life. Regale bought three Mercedes-Benz sedans; paid $300,000 toward a $570,000, seven-month rental of a beach house in Naples, Florida; and took at least three Lear jet trips between there and Grenada, at $30,000 per flight. Barnabe paid $350,000 for a 2000 Carver 350 Mariner yacht that he named Offshore Funs. Skirving used a $183,000 check from an investor to make a partial down payment on a $1.3 million home in Clackamas. They bought tanning beds and jewelry and went on gambling sprees.

Barnabe even persuaded Grenadian authorities to launch an “Economic Citizenship Program,” in which, for $250,000 paid to the government coffers, anyone could receive a Grenadian passport. Ziegler bought one and also gave himself a dapper new name: Van A. Brink. For Ziegler, it was a smart investment, as having two names and as many as three passports made it easier for him to travel abroad to make his pitch and hand out literature that read, “It’s that simple. Buy low. Sell high.” Ziegler often read the line aloud to his audience, so people knew exactly what they were getting into.

Marchant, the OffshoreAlert publisher (he’s been called “the offshore pit bull”), first heard about First Bank from a friend. “I took a look, and it was obvious it was a scam,” he says, speaking from his offices in Miami. “Anytime any bank offers a guaranteed high rate of return it’s a fraud, with no exceptions whatsoever.”

Of the thousands of offshore banking schemes that Marchant has tracked and covered in his newsletter, he calls First Bank the most audacious. “None of [the ringleaders] were bright,” he says, “but they had no sense of shame, no social conscience, they were not held back by any sense of ethics…. And why did it succeed? Because an entire jurisdiction welcomes them with open arms.”

The man charged with regulating Grenada’s offshore banking industry was Michael Creft, a Grenadian who had worked in Canada for two decades, most recently as a policy analyst with the Manitoba Department of Highways and Transportation, before returning to his home country in August 1997 to accept the newly minted job of Registrar of Offshore Services. Creft was the one charged with, for example, verifying that First Bank had the required $2.25 million in capital and collecting the bank’s quarterly audit reports. Every time Creft inquired about the reports, Ziegler and his staff delivered excuses: We are just so busy hauling in millions, we haven’t had time to compile them, and couldn’t Creft just wait a bit? First Bank was, after all, contributing to Grenada’s economy by buying office equipment, cars, and real estate, and by employing Grenadians. So yes, Creft could wait, and while he waited, he wondered whether First Bank might consider a $20,000 campaign contribution to Grenadian Prime Minister Keith Mitchell. First Bank agreed, as it did to other five-figure “donations” to various officials. When Creft’s car broke down, First Bank made a $1,000 payment to a local garage.

At one point, to prove that First Bank actually held the assets it claimed, the bank produced a faxed copy of an appraiser’s report “proving” the bank owned a 10,000-carat ruby carved in the shape of a boy riding a water buffalo, a gem worth $20 million. There was also a certificate from the Union Bank of Switzerland that was supposed to prove First Bank owned 870 kilograms of gold bullion, even though First Bank’s name appears nowhere in the paperwork. (On the document, “collectible” is spelled “collactable.”) Creft accepted these as proof the bank at least was solvent.

Others were not as credulous. In January 1999, Marchant exposed First Bank in his newsletter, calling it a “massive fraud” and writing, “the IDIC scam is a carbon copy of a fraud perpetrated by the European Union Bank of Antigua that collapsed in 1997.”

First Bank and the IDIC sued Marchant for libel in US District Court in Miami. “One of the most outrageous conclusions offered by OffshoreAlert is that First Bank … is a Ponzi scheme…. Does the simple offering of high yields to depositors constitute publishable proof that such a bank is operating a Ponzi scheme?” Ziegler wrote in an affidavit filed in Grenada. One of the documents produced in First Bank’s defense was a letter from Creft exonerating First Bank of any wrongdoing. (The letter concluded, “Reckless smear campaigns hurt not only offshore companies but also the Government and people of Grenada and casts aspersions on the integrity of our jurisdiction.”) Ultimately, the court dismissed the suit.

But the impact of the article was immediate. More and more investors, panicked over losing their life savings, started calling the Young Street offices demanding to know what happened to their interest checks.

In October 1999, with Marchant beating his drum, with Nevis’s Ministry of Finance demanding that the IDIC shut its doors on the grounds that it was a sham insurance corporation, with investors clamoring for money, Ziegler decided to resign as First Bank’s CEO. He packed up and moved to Uganda, where he bought a $1.3 million walled compound with a pool and a squash court on the outskirts of Kampala. In a story about the bank’s troubles in the Wall Street Journal, Ziegler responded to a reporter’s questions by e-mail: “The truth is that it isn’t very popular to be so successful when you’ve had such a checkered past,” he wrote. “Maybe it is just that the lower and middle classes are much more understanding of someone who has suffered setbacks, learned from them and figured out how to move on and share what he has learned with others. Or maybe I’m just a sociopathic con artist who needs to be put away.”

On August 11, 2000, the Grenadian Minister of Finance appointed an administrator to oversee First Bank; he subsequently ordered the bank to provide proof within seven days of “the assets you say are owned by the bank, I believe the last count was $62 billion.” The bank could not, and on February 15, 2001, Grenada revoked First Bank’s license.

Marcus Wide, a partner with PricewaterhouseCoopers from Halifax, Nova Scotia, arrived at First Bank’s Young Street offices in March 2001. An expert in untangling complex financial webs, Wide has worked on some 35 offshore banking investigations during his career—all but one of which was a sham. “You also have to remember, these islands were not very far from colonialism, and the first generations, very bluntly, were prone to corruption,” he says. “They were so poorly regulated and so poorly supervised, it was an invitation for the crooks to move in.”

Hired by Grenada to calculate and liquidate First Bank’s real assets, Wide and his team spent some three months digging through more than 200 boxes of paperwork and thousands of documents—all that was left in the bank’s wake.

The 10,000-carat ruby that the bank reportedly owned did exist—but it belonged to a California man who had never heard of Ziegler or First Bank. The 870 kilograms of gold bullion were a lie. Wide also found fake checks from fake banks, fake checks from real banks, and thousands of documents that led nowhere. After a month, he released the first of what would be a three-part, 163-page liquidation report. First Bank, he wrote, “was and remains a sham.” Wide eventually determined that First Bank had bilked people out of at least $170 million.

As far as the bank’s recoverable assets, he calculated that the billions of dollars First Bank often claimed it possessed came to no more than $2 million. There was nothing to recover for the people who had entrusted First Bank with their money.

“People did not want to believe that these massive yields were in fact a fantasy,” Wide said recently from his home in Halifax, adding that even after the bank closed, investors continued to call Grenada, insisting that there must be some mistake. “But after I got in there, and it became known there was a liquidation going on,” he says, “the silence was almost deafening.”

Soon after First Bank was shuttered, Ziegler went on to start a new scam: an e-mail campaign known as the Restoration Project. In it he pleaded with people who had sent money to First Bank, asking them to reinvest so that he could fight Wide and PricewaterhouseCoopers, whom Ziegler accused of wresting control of the bank.

Ziegler had a line on a secret project, the e-mail read, involving multimillions and even billions of dollars. For every dollar he received, Ziegler promised a return of $200, and if people signed up right away, their names would be put at the top of the list for repayment. “And the alarming thing is that Ziegler managed to raise some more money,” says Wide. “Of course, he just pocketed the money again.”

Closing First Bank was relatively easy, but actually convicting the ringleaders of money laundering was another matter entirely. Before the US Department of Justice could bring charges against Ziegler, Barnabe, Ferguson, Regale, and Skirving, it needed solid evidence against the group—prosecutors needed to be able to trace precisely how the group stole, laundered, and then spent its millions of dollars.

Leading the grand jury investigation was Assistant US Attorney Claire M. Fay, who took the case in October 1998 and started following the money. She knew from speaking to investors that they’d sent their checks to an address in Antigua, checks made out not necessarily to First Bank but to a number of fund names. Once the money reached Antigua, a Ziegler employee would stuff the checks into an envelope and mail them back to the States, to a small check-processing company called Automated Payment Processing (APP), located in a Forest Grove office building. APP, in turn, deposited the checks into its own legitimate bank account at a nearby branch of US Bank. “Then they just waited for [disbursement] instructions from Brink and Regale,” says Fay. The pair then directed the now-laundered funds to various overseas accounts. Because of APP’s affiliation with offshore banking, US Bank eventually asked the company—which was oblivious to the illegality—to shut its account. But that hardly impeded First Bank’s activities: Fay soon discovered that First Bank employed check-processing centers in Washington State, Nevada, St. Vincent, Nevis, Uganda, and the Isle of Jersey.

What she really needed to convict Ziegler and his cohorts was evidence from Grenada—which turned out to be extremely difficult to obtain, in spite of the many grand jury subpoenas issued by the Department of Justice. When the department sent one to Ferguson requesting IDIC records, for instance, his response read, in part, “It was a policy that all correspondence was shredded and e-mails deleted after being read … not for any sinister purpose, but to meet the contractual provisions for total confidentiality.”

She also had a difficult time getting testimony from investors, many of whom were embarrassed that they had been scammed or who still held out hope that First Bank would eventually come through with their money. “We got the equivalent of doors slamming in our faces, [people] saying, ‘We’ve signed nondisclosure agreements as part of our investment, and we can’t talk to you.’”

In 2002, after Wide had completed his report, Grenada finally released First Bank’s papers to Fay. There were 223 boxes that were covered in mold. A hurricane had hit Grenada in the interim, and the papers inside were yellowed, wavy, and dank. “The smell of these records—it was terrible!” says Fay. And then she began the long, tedious task of trying to make sense of what happened. “I was Alice down the rabbit hole…. The first document might look legitimate, and it might purport to be secured by a second document, which is secured by a third document, and you have to go to the third or fourth level before you find the thing that’s just a completely bogus forgery.”

While Fay was building her case, the First Bank players got back to work. Skirving proposed to Ziegler and Ferguson that they open another bank in Grenada. (“The new name could be ‘First Bank of the Caribbean’ or something like that,” he wrote in an e-mail.) Instead, Skirving started the Bank of the Nations, a nonexistent bank that he ran from Portland using many of the same lures as First Bank. (In 2002, the Oregon Department of Consumer and Business Services sued the partners of Bank of the Nations; in 2005, Multnomah County fined them more than $2.3 million.)

In Las Vegas, Barnabe gave seminars to potential offshore investors and worked on a new bank that would issue “gold-backed” CDs. And from Uganda, Ziegler continued to push the Restoration Project. “They never met a scam they didn’t like,” says Fay, noting that revictimizing people is a hallmark of the con man. “They prey on the victim who thinks, ‘Oh gee, if I just send X amount of dollars, all will be well, I’ll get my money back, I won’t have to suffer either this financial loss or this huge humiliation…. ’ We sent out thousands of questionnaires to people, trying to locate as many [victims] as we could.” Only a couple of hundred came back.

Eventually, Fay had enough evidence to bring money-laundering charges against the First Bank group. On January 6, 2004, FBI agents arrested Skirving and Barnabe outside Las Vegas, and Regale in Naples, Florida. Ferguson, however, had moved into Ziegler’s compound in Uganda, where they had started another plea for funds called “Staying Alive Money,” or SAM. The US Department of State revoked the men’s American passports; Interpol, the world’s largest international police organization, issued a fugitive alert.

On May 28, 2004, five FBI agents waited at Entebbe International Airport as Ugandan police encircled Ziegler’s estate. When the police crashed through the door, one of Ziegler’s bodyguards pulled a gun; the police shot and killed him before apprehending Ziegler and Ferguson. The men were flown in handcuffs to Johannesburg and then to the United States, where they eventually joined Regale, Barnabe, and Skirving in the Multnomah County Inverness Jail. They spent between three months and a year there, pending trial.

Three years after their arrests, on August 27, 2007, in US District Court in Portland, the First Bank crew were finally sentenced for their financial crimes. Barnabe was sentenced on charges of selling unregistered securities; he’s now serving six years in the California City Correctional Institution. The others were sentenced on charges of money laundering. Ferguson received four years, four months, which he is serving in the Federal Correctional Institution in Sheridan, Oregon; Skirving’s there, too, serving eight years, one month; and Regale is serving her 18 months in the Federal Correctional Institution in Coleman, Florida.

Ziegler, however, served no time. On December 10, 2005, he died of a massive heart attack at his former brother-in-law’s house, while awaiting trial.

Ferguson declined a face-to-face interview for this article, but he wrote a brief letter about First Bank from prison, indicating that his involvement is “more a case of being in the wrong place, etc.” When contacted, Barnabe declined to be quoted. His daughter, however, defended her father in an e-mail. “I believe there are some individuals that are accountable to this tragic situation, but know that my father was used as a ‘scapegoat’ in this case. I can tell you he is a man of integrity…. ”

Shortly before Ziegler’s death, he wrote his version of events, a letter that now appears on a message board of the OffshoreAlert website. In it, Ziegler paints himself as the hero of the First Bank story, which he likens to an espionage thriller. He claims that he was forced to leave Grenada in order to locate a vault in which to store the 870 kilograms of gold the bank still owns, as well as $300 million in pre-1935 US currency. He describes plans to broker peace accords among African tribal kings and to build a new bank in Uganda, one that will certainly require razor wire, armor-plated walls, and electronic surveillance, because now he is the target of an assassination plot. In order to save First Bank, he had to jet around the world—to Japan and South Africa and Cuba—an odyssey that has “fully become a surrealistic nightmare that would have done Rod Sterling [of ‘The Twilight Zone’] more than proud.” But soldier on he does—in order to recoup all of his investors’ losses, in order to build an even better bank. He assures people that he has a lock on another $21 billion in financing.

In an episode of the CNBC series American Greed that aired earlier this year, Ziegler can be seen in a grainy video from First Bank’s heyday, flashing a gap-toothed grin at his audience. “What you’re involved in is a banking concept that has absolutely that many people with big banking credentials and previous experience,” he says—“that” meaning the zero he makes with his thumb and forefinger.

It is perhaps the one time that Ziegler was telling the truth.